All Categories

Featured

Table of Contents

Keep in mind, nevertheless, that this doesn't say anything regarding adjusting for rising cost of living. On the bonus side, even if you assume your choice would be to buy the securities market for those seven years, which you would certainly obtain a 10 percent annual return (which is far from particular, particularly in the coming years), this $8208 a year would be more than 4 percent of the resulting nominal stock value.

Example of a single-premium deferred annuity (with a 25-year deferral), with 4 settlement choices. The month-to-month payment right here is highest possible for the "joint-life-only" alternative, at $1258 (164 percent higher than with the immediate annuity).

The means you buy the annuity will determine the solution to that concern. If you buy an annuity with pre-tax bucks, your premium lowers your taxable income for that year. According to , buying an annuity inside a Roth plan results in tax-free payments.

How can an Deferred Annuities help me with estate planning?

The expert's very first step was to develop an extensive financial prepare for you, and afterwards clarify (a) exactly how the suggested annuity suits your overall strategy, (b) what alternatives s/he taken into consideration, and (c) how such alternatives would certainly or would not have caused lower or greater compensation for the expert, and (d) why the annuity is the premium choice for you. - Tax-deferred annuities

Certainly, an expert may try pushing annuities even if they're not the best fit for your circumstance and goals. The factor might be as benign as it is the only product they market, so they fall prey to the typical, "If all you have in your toolbox is a hammer, rather quickly every little thing starts resembling a nail." While the consultant in this scenario might not be dishonest, it raises the risk that an annuity is a bad choice for you.

What are the top Secure Annuities providers in my area?

Since annuities often pay the agent selling them much higher compensations than what s/he would obtain for investing your cash in shared funds - Retirement annuities, not to mention the no payments s/he would certainly obtain if you purchase no-load common funds, there is a big incentive for representatives to press annuities, and the extra challenging the far better ()

An unscrupulous expert suggests rolling that quantity into new "much better" funds that just occur to carry a 4 percent sales tons. Accept this, and the advisor pockets $20,000 of your $500,000, and the funds aren't most likely to execute far better (unless you picked a lot more poorly to start with). In the very same example, the consultant might guide you to get a complicated annuity with that said $500,000, one that pays him or her an 8 percent payment.

The advisor tries to rush your decision, claiming the offer will certainly soon go away. It might undoubtedly, however there will likely be equivalent deals later on. The consultant hasn't identified just how annuity settlements will be exhausted. The advisor hasn't revealed his/her compensation and/or the charges you'll be charged and/or hasn't shown you the effect of those on your eventual payments, and/or the settlement and/or charges are unacceptably high.

Your family background and present wellness indicate a lower-than-average life span (Secure annuities). Present passion rates, and thus predicted repayments, are historically reduced. Also if an annuity is right for you, do your due persistance in contrasting annuities offered by brokers vs. no-load ones sold by the releasing company. The latter may need you to do even more of your very own study, or utilize a fee-based economic advisor that may obtain compensation for sending you to the annuity issuer, but may not be paid a greater payment than for various other financial investment alternatives.

Retirement Annuities

The stream of monthly settlements from Social Safety is similar to those of a delayed annuity. A 2017 relative evaluation made a thorough comparison. The following are a few of one of the most significant factors. Since annuities are volunteer, the people getting them typically self-select as having a longer-than-average life expectations.

Social Safety benefits are fully indexed to the CPI, while annuities either have no inflation protection or at the majority of provide an established percentage annual boost that might or may not make up for inflation in complete. This sort of rider, as with anything else that increases the insurer's risk, needs you to pay more for the annuity, or approve lower settlements.

How long does an Annuity Contracts payout last?

Disclaimer: This write-up is meant for informational objectives only, and must not be considered economic recommendations. You need to get in touch with an economic professional before making any major financial choices. My profession has actually had lots of uncertain weave. A MSc in academic physics, PhD in speculative high-energy physics, postdoc in bit detector R&D, study placement in speculative cosmic-ray physics (consisting of a number of visits to Antarctica), a short job at a little engineering services business supporting NASA, followed by beginning my own small consulting technique sustaining NASA tasks and programs.

Considering that annuities are intended for retired life, tax obligations and penalties might use. Principal Defense of Fixed Annuities. Never shed principal as a result of market performance as dealt with annuities are not bought the market. Also throughout market downturns, your cash will certainly not be affected and you will not shed cash. Diverse Investment Options.

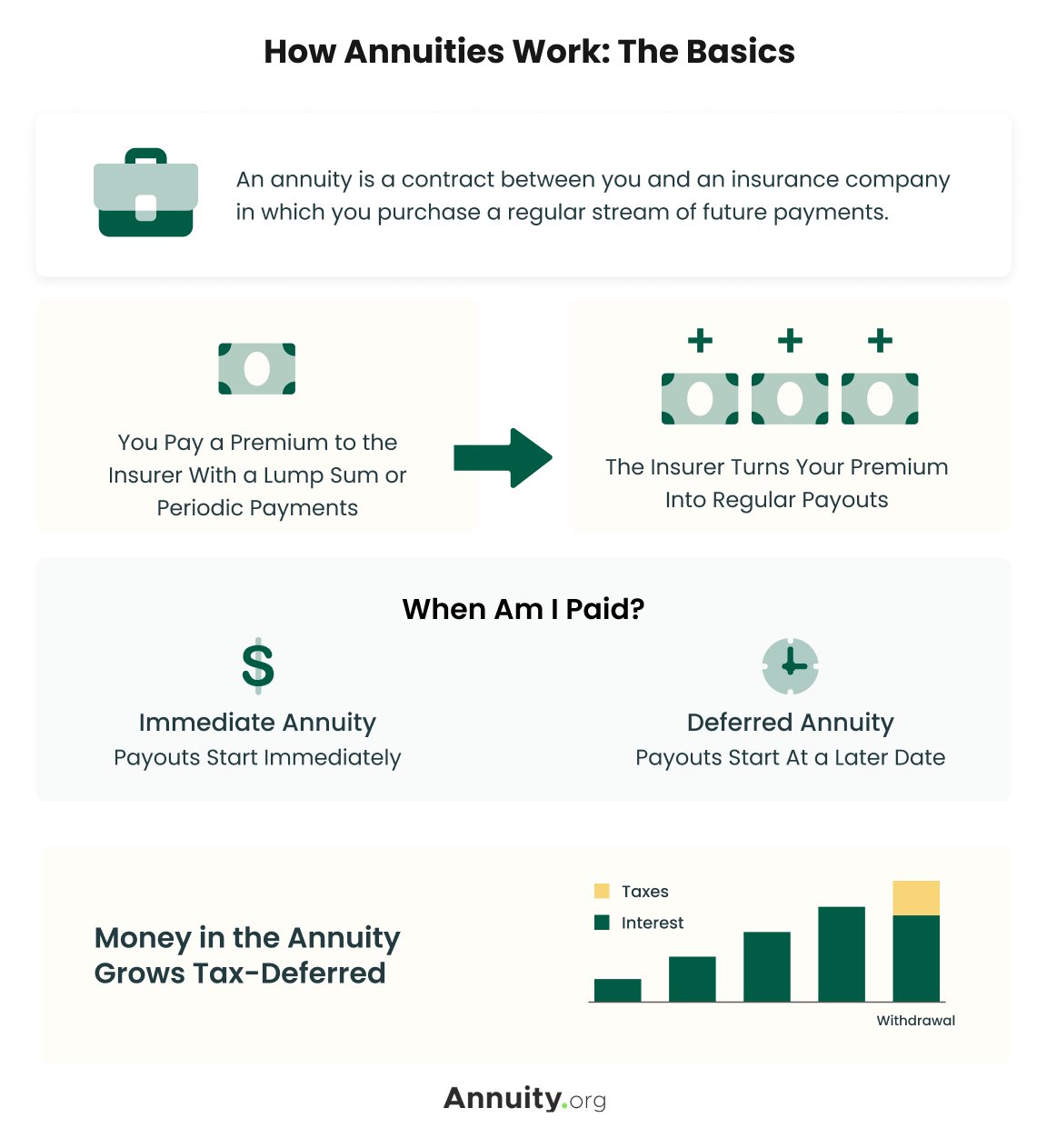

Immediate annuities. Utilized by those that want dependable revenue right away (or within one year of acquisition). With it, you can customize revenue to fit your needs and create income that lasts permanently. Deferred annuities: For those who wish to grow their money gradually, but agree to delay accessibility to the cash until retired life years.

Where can I buy affordable Annuity Contracts?

Variable annuities: Gives greater capacity for development by investing your cash in investment choices you select and the capability to rebalance your profile based on your preferences and in such a way that aligns with transforming financial goals. With fixed annuities, the business spends the funds and provides an interest price to the client.

When a death claim occurs with an annuity, it is vital to have a called beneficiary in the agreement. Various options exist for annuity death advantages, depending upon the agreement and insurance firm. Selecting a refund or "period particular" alternative in your annuity supplies a survivor benefit if you pass away early.

What is the process for withdrawing from an Fixed Annuities?

Naming a recipient various other than the estate can assist this procedure go much more smoothly, and can aid make certain that the earnings go to whoever the specific desired the cash to go to rather than going through probate. When present, a death benefit is immediately consisted of with your agreement.

{kind=link}

Latest Posts

Who has the best customer service for Annuity Interest Rates?

How do I apply for an Lifetime Income Annuities?

How do I apply for an Long-term Care Annuities?